Location: The Pierre, New York City Partner: BDO (www.bdo.com)

JEGI CLARITY held its second Executive Leadership Dinner of 2023 on May 31st at the Pierre in New York starting at 6PM with cocktails. These events are structured as roundtable discussions and provide a stimulating evening of great conversation and networking.

This Dinner was titled “How The Business Of Legal Services Is Changing And Why PE Is So Excited About It.” The roundtable discussion was led by Matt Sunderman, Chief Executive Officer of HBR Consulting + LAC Group + Wilson Allen, who shared his perspectives on the evolving legal services landscape, the impact of AI on the legal profession, and trends in both the business and practice of law as well as private equity and other non-lawyer ownership.

The Dinner brought together approximately 35 senior executives from a mix of large global corporations and emerging companies.

Building MiQ, the Leading Global Programmatic Media Partner

JEGI CLARITY’s 19th Annual Media & Tech Conference focused on ‘Maintaining a Winning Mindset,’ brought together senior executives and investors from across the global media, marketing, information, and technology sectors.

At the conference, Marcus Anselm, a Partner from JEGI CLARITY’s London office, interviewed Gurman Hundal, CEO & Founder of MiQ, a leading programmatic media partner to the world’s largest brands and agencies.

In H2 2022, MiQ received an investment from private equity firm, Bridgepoint, which valued the company at nearly $1Bn, generating a 6.1x return for its previous investor ECI Partners. JEGI CLARITY had the pleasure of advising Bridgepoint on the transaction. During their fireside chat, Marcus asked Gurman about the journey he had been on since the business was co-founded in 2010 and its transformation into the major global player it is today. Gurman shared his views on topics ranging from how the business started out and how to build the best relationship with private equity firms to future trends in the AdTech space. We’ve picked just a few highlights from the thought-provoking session.

From ‘bootstrap‘ beginnings to private equity funding

Gurman and the Co-Founder & Global Chief Growth Officer of MiQ, Lee Puri, started the company in the UK without any external funding, investing $20,000 each at its genesis. Within a few months they had a revenue of $100K and $20,000 in EBIT which they reinvested to grow the business. Early challenges included building a business in South India to provide the right technical expertise for their service and breaking into the US market.

Up until that point, growth had been entirely organic, but it was an offer to buy the business that Gurman and Lee walked away from in 2016 that led to them to think about partnering with a PE firm. It challenged the misconception they had previously held about what it would be like, and the value that an investor could bring to them. When asked about the advice he would give both to an agency thinking about bringing in a PE partner, Gurman advocated spending a lot of time getting to know one another, ensuring the culture is right. From the PE firm’s point of view, he advised that it was vital to take the time to understand the complexities of the fast-moving AdTech industry. For agencies, he advised that a good PE partner “should be an extension of your leadership team, you should want to pick up the phone to them.”

The power of retention – clients and talent

In the face of a talent shortage, Marcus asked how they keep retention rates well above 80% at MiQ. Gurman explained that two main areas of focus for the business were retention of clients and retention of talent. At the start of the pandemic they made a promise not to fire or furlough any employees. They worked hard to listen to what their employees wanted and tracked employee engagement religiously. Gurman stated that he and Lee have been “relentless about the people experience. At the end of the day as Founders that’s our legacy – how people felt when they worked at MiQ, that’s what we care about the most. Ultimately, I believe if you care about that the most, you tend to have a good business.”

Next stage for growth

The conversation then turned to growth for MiQ and current market sentiment. Gurman commented that although the market was still volatile, programmatic advertising, because of its flexible and responsive nature, was well positioned. Brands, as ever, are interested in how they are reaching users, they want to follow the ‘eyeballs’ and behavior. Gurman predicted the continued rise of digital at home among other platforms and there was real interest in how opportunities in home game consoles might develop as well as branding in games.

In response to Marcus’ question about what is next for MiQ, Gurman said he believed there was still more opportunity for organic growth – which could lead to them doubling the size of the business. He also talked about their new M&A capability, which completed its first deal earlier this year and will provide MiQ going forward with “the muscle to be a strategic buyer in the AdTech space.”

For more information about our conference please click here.

Cannes Lions celebrates, facilitates, and substantiates creativity in all its forms – helping to prove its effectiveness, shape its future, and connect the future leaders of the industry.

As longstanding advisors to this community, we continue to deliver numerous landmark transactions across the Global Advertising, Marketing and Communication sectors.

Contact Marcus Anselm or Jonathan Davis to arrange a meeting to discuss M&A in the sector as well as explore how we might be useful to you and your business.

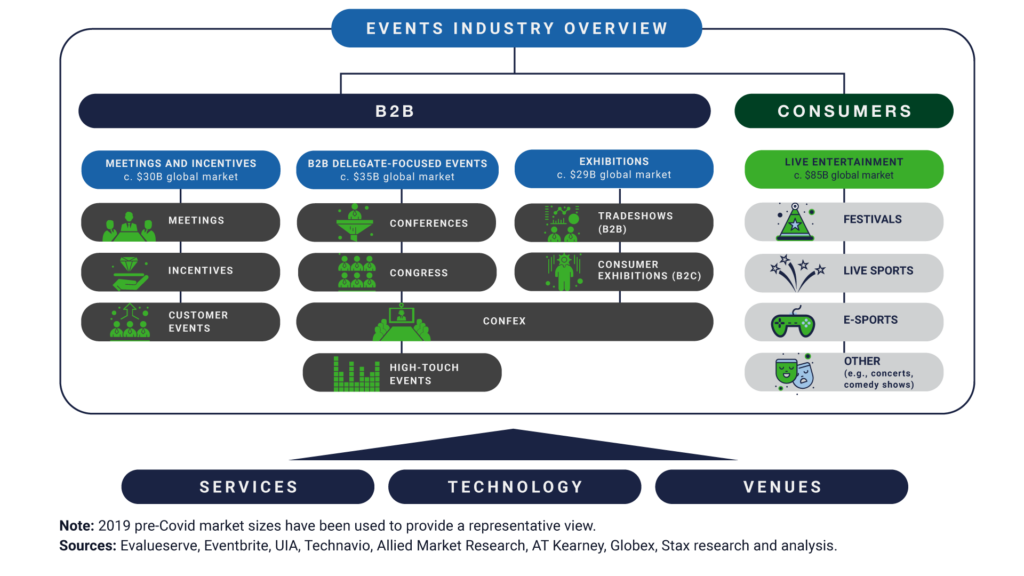

The events industry has bounced back faster than expected, its value has been proven and even strengthened by Covid. Investors are jumping back in to access deal opportunities across the size spectrum in the ecosystem.

Renewed importance of a diverse industry

Three years ago, Covid brought the world to a complete halt and the Face-to-Face (F2F) industry, be it exhibitions, tradeshows, conferences, 1-2-1s, experiential events, or corporate events, was one of the most affected sectors. Today, the F2F industry is seeing renewed importance as attendees are flocking back to all forms of events with irrefutable energy and motivation.

Event participants have a heightened appreciation for the value and unique advantages of meeting F2F in environments that foster networking, building new relationships, collaboration, and a more focused learning environment. Net Promoter Scores (NPS) evidence this. Pre-pandemic, industry benchmarks put average visitor NPS in the +5 to +7 range, with average exhibitor NPS being negative. Explori reported a post-Covid increase of 20 points in the NPS average in 2021 as F2F resumed. With these higher levels of engagement and satisfaction among attendees, sponsors and exhibitors are also reaping the benefits and strengthening their commitment to the category. A Stax survey of 196 sponsors of corporate events showed an uplift of 29% in perceived value of events from 2019 to 2023, with net sentiment increasing from slightly positive to positive. More broadly, the shift to remote and hybrid work has created an environment where F2F is significantly more valuable now for selling, marketing, and networking as well as for corporate team building, strategy, engagement, and culture. These positive views are here to stay.

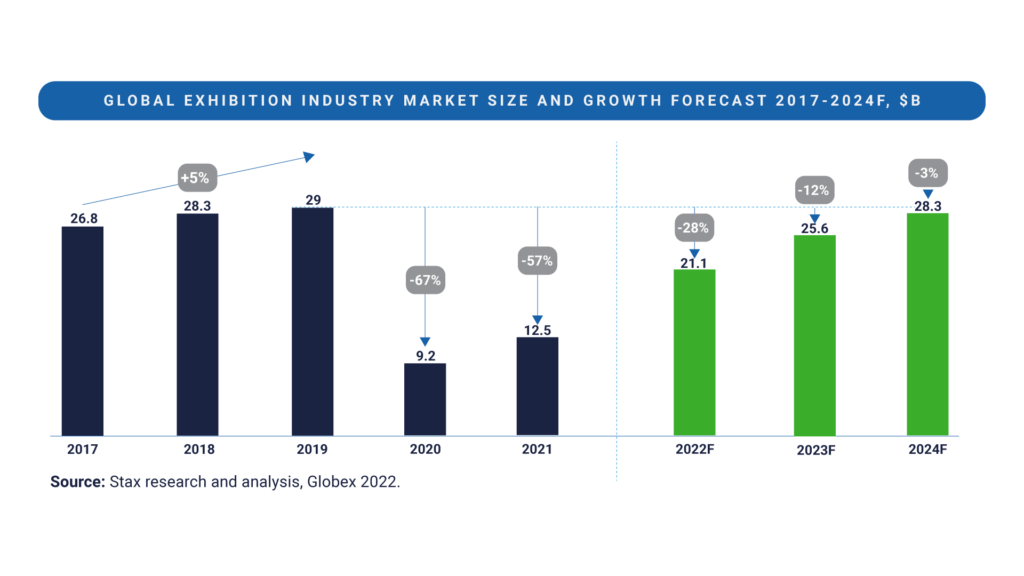

Full recovery of market size

The global exhibition organizing market has traditionally grown ahead of GDP, for example, growing at 5% annually from 2017 to 2019 when it reached a total value of $29B. But Covid halted this growth dramatically in its tracks, with the market shrinking by 69% to $10B in 2021.

With Covid re-proving and even enhancing the value of proximity and immersion brought by F2F, near-full recovery is forecast in 2023. Growth is established at or above pre-pandemic levels and the industry will look much the same. F2F remains the core, now enhanced by the accelerated development of adjacent digital products and data during Covid, providing potential for deeper reach into the communities served by event brands.

Beyond exhibitions, the recovery and growth rates of other segments of F2F such as meetings & incentives and delegate-focused events are mirroring or even outperforming the sector. In addition to organizers, service providers to the industry such as contractors and other suppliers are also benefiting strongly from the return and can expect continuing growth.

This bounce-back has not been universal, however. Asia has been restrained by China’s zero-Covid policy, but that market has now reopened. Domestic growth in China will continue, but organizers will look at other trade flows for event participation. Smaller, weaker events are not returning, but we are seeing a substantial increase in event launch activity as organizers target emerging sectors, mostly with a tech focus.

The rationalization of virtual

The pandemic highlighted the analog nature of the industry, with only 2% of digital revenue in 2019. The emergency dash to digital brought some success and innovation, but limited monetization. Efforts were mostly failures, most of the stopgap efforts were not repeated.

While digital technology allowed us to stay connected and continue to do business during difficult times, we now have the proof-point that virtual events cannot fully replace the real human connection that helps brands build visibility and trust. Only a small set of events such as some delivering training and educational content have remained exclusively online now that it is possible to meet in person again.

Coming out of the pandemic, we are seeing the number of virtual platforms decreasing. When Covid hit many event organizers scrambled to shift their in-person offerings to virtual. Now we are seeing rationalized offerings that augment F2F, extend engagement to 365, and provide opportunities for performance-based marketing, broader content engagement, data collections, and analytics. Digital revenues will not expand as rapidly as predicted in the pandemic, but we expect them to grow at double-digit CAGR to contribute over $1B by 2024, substantially up from the pre-Covid levels of c.$650M. Much of this will be driven by the monetization potential of standalone offerings that extend F2F exhibitions (e.g., 365 year-round digital services, marketplaces, newsletters) being realized.

Transformation to community and customer value

Although events have proven value standing alone, winning organizers had already embarked on a journey of transformation before the pandemic, recognizing the need and opportunity to give customers greater value. Informa’s IIRIS data strategy is a major investment in customer closeness. Italian Exhibition Group announced its community catalyst strategy, others are taking similar initiatives .

We also see other changes to business models, mostly driven by acquisition. Emerald’s acquisition of Bulletin complements its NY gift fair and makes a serious entry to marketplaces. Organizers Clarion, Hyve, and Tarsus have all acquired businesses that organize one-to-one meetings, seeking to spread that competence across their portfolios. Overall, the industry is evolving towards greater use of data and technological integration, allowing it to increase market reach and audience involvement.

Transactions are back

With F2F back on track to pre-pandemic levels and the industry stronger, investor confidence has also returned. This is shown by the slew of major and some smaller deals in 2023, proving that the industry is both attractive and investable.

The industry is seeing a return of M&A activity and relatively strong transaction multiples. North America continues to lead the way with a strong market recovery post-Covid and a broad set of actionable opportunities. In 2020, North America saw 88 event-related transactions, followed by 94 in 2021 and 106 in 2022. Europe has also recovered well and has seen a similar M&A pattern with 90 event related transactions in 2020, followed by 98 in 2021 and 96 in 2022. M&A activity in the APAC region remains subdued.

In addition to mainstream traditional events that have rebounded, buyers are looking to acquire “tip of spear” and other innovative business models which enable higher sales conversion and more efficient buyer engagement. These include smaller curated events that occur throughout the year such as 1-2-1 and hosted-buyer events, content-rich conferences delivering critical information to their communities, and focused knowledge-sharing businesses, such as peer-to-peer networks. Investors have the strongest appetite for growing, resilient, global verticals such as healthcare and technology. Given the current macro-economic backdrop they are less focused on cyclical markets such as construction and retail, although software and tech that is driving productivity in any market is a hot topic.

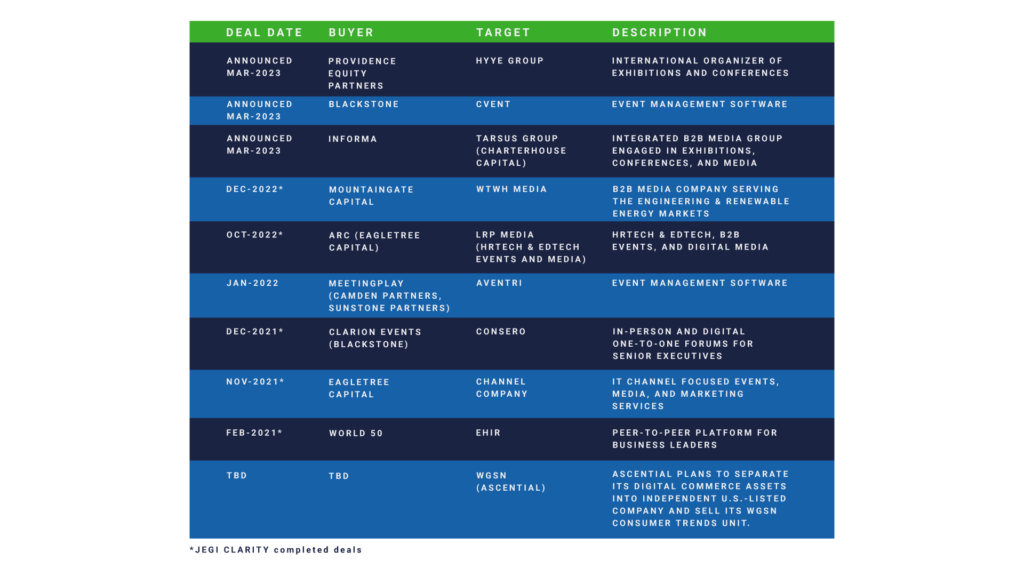

At the end of 2022, the F2F industry saw notable activity. JEGI CLARITY was the sell-side advisor on three event-related transactions in Q4 2022: LRP Media Group’s sale of its HR Tech and Ed Tech B2B event and digital media portfolios to Arc, backed by investment funds managed by EagleTree Capital; e.Republic, a media, research, data and events company, sale to Leeds Equity Partners; and the investment in WTWH media, an integrated B2B media company that includes 12 events, by Mountaingate Capital.

Fast forward to March 2023, the industry saw three large and transformative acquisition announcements. Informa plans to acquire Tarsus, operator of 160+ B2B event brands, for $940M. Less than a week later, Blackstone, a fund focused on events and travel recovery, announced it has entered into a definite agreement to acquire meetings, events, and hospitality tech provider Cvent for $4.6B. Shortly after, Providence Equity Partners, partnering with Searchlight Capital Partners announced that they had made an offer to acquire Hyve Group, a U.K. event organizer for $579M, approximately 20.3x EBITDA for FY22.

Stax has been equally busy over the past 12 months with six sell-side and buy-side commercial due diligences across exhibitions, conferences, and experiential, as well as its other strategy and transformation work in F2F.

Select deals in F2F

We will also see a wide range of investment opportunities in the broader ecosystem beyond event organizing. Service providers that support organizers are now in a stronger position than pre-Covid. Building from their downsized bases, these providers are enjoying strong growth in line with the faster than anticipated industry bounce-back. With some scarcity of supply, many players are able to command higher prices from customers and improve margins.

The $4.6B Cvent investment underpins the attractiveness of technology players that support meeting and event organizers as well as their participants. In venues, while there is overcapacity in some parts of the world, the value or specialized, flexible pace is highlighted by Convene’s investment in etc.venues.

Further investment ahead

With continuing positive fundamentals, we can expect to see more transactions throughout the ecosystem. Private equity investors such as Blackstone, Providence, Charterhouse, EagleTree, and others have made strong returns repeatedly across a number of deals. They will be joined by others attracted by the quality of the industry’s fundamentals and its recovery.

Global Digital Services Market The Investment Opportunity

Overview

JEGI CLARITY has been a prominent player in the Marketing, Content and Digital Services sectors for over three decades. During this time, we have witnessed significant changes in the industry, none more so than what we are experiencing in the Global Customer Experience market today.

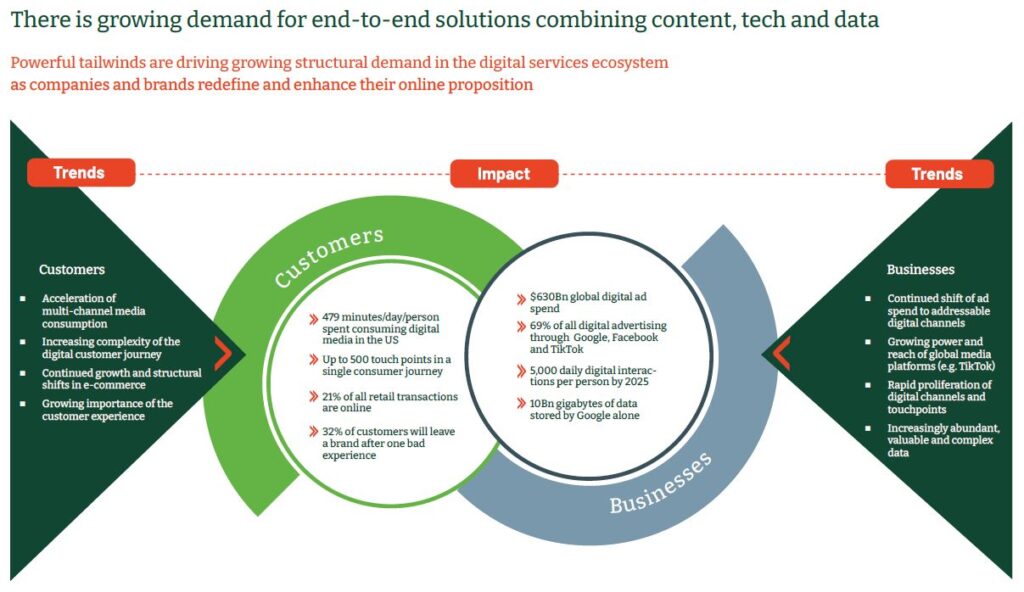

As our report indicates there are powerful tailwinds driving structural demand in the digital services ecosystem as companies and brands redefine and enhance their online propositions. The market is now estimated to be worth over $100 billion in the US and UK alone and showing strong growth despite broader market conditions.

As a consequence, there has been a sharpened focus from the Private Equity community over recent years attracted by the high single-digit, low double-digit money multiple returns that their peers have achieved. As the wider M&A market starts to warm up, we anticipate several PE-backed platforms will be in play over the next 12 to 24 months driving further investment into and consolidation of a highly fragmented industry.

Larger strategic players, such as Accenture Song, Wipro, and WPP, are also actively looking to add to their capabilities by consciously building integrated offerings on a global scale.

Whether you are a corporate looking to ramp up investment or a Private Equity firm seeking to participate in this market opportunity, we would be delighted to share our comprehensive report and provide you with a more detailed account of the sector. Contact us at globaldigitalmarket@jegiclarity-emea.com.