Patricia Vicente (Director, EMEA) and Jonathan Goodale (Chief Business Development Officer, EMEA) attended Mobile World Congress (MWC) in Barcelona, Spain.

The event remains the largest Mobile Technology and ‘Connectivity’ gathering globally, and we were particularly focused on meeting businesses across the Mobile Software and Services ecosystem as well as learning more about new innovations and topics occupying decision makers in 2023.

Below are some of our key takeaways from the event:

Velocity was the conference’s theme this year, a positive message in a time of mixed political and macro factors and signaling that the pace of technological innovation and demand for digital experiences has not been muted.

With an estimated 80,000 attendees the event was back to nearing pre-COVID interest levels.

Unsurprisingly there was much talk about the Metaverse and Web 3.0, particularly questions around what happens if we do arrive at a consumer adoption tipping point for the technology, and how the current 5G infrastructure will cope.

Cue whispers of 6G; the next generation of mobile infrastructure. However, with a planned roll out no sooner than 2030, questions remain as to whether we would logistically be ready for mass Web 3.0 adoption in the near term.

Artificial Intelligence (AI) and ChatGPT were also front of mind for many. All players we spoke with, including corporates/brands, tech vendors as well as service providers, are toying with what it means for them. One vendor we spoke with who provides App Store Optimization tools to global brands is looking at using AI/ChatGPT to allow their product to make decisions for customers rather than just prescriptions based on data and analytics. Clearly for this type of tool to work, it relies on customers trusting the technology and it will be fascinating to see how far into decision making AI automation will be allowed to go.

The impact of macro and political events on the mobile tech world and its supply chain was more evident than ever this year. S4 Capital’s Chairman and WPP Founder, Sir Martin Sorrell commented on how companies are having to reconsider supply chain and workforce distribution carefully in the face of global political uncertainty.

The 4YFN (4 Years From Now) startup arena was full of innovative young businesses alongside earlier stage investors from across the world. The 4YFN Startup Award was won by Spanish employee payment technology provider Payflow whose salary advance platform aims to improve the employee experience and allow financial flexibility for workers through technology.

General sentiment was that investment in start-ups is still active but more selective with founders and owners needing to demonstrate they are prepared and ready for investment to differentiate themselves from the crowd.

As The Metaverse adoption continues apace, there will be an unprecedented wall of expertise required to service demand

Author: Jonathan Davis, Partner, EMEA

For all the recent publicity, “The Metaverse” remains a relatively opaque concept. Perhaps the simplest way to think about it is as the potential cyberspace functionality provided by Web 3.0 (the name that signifies the third generation of the Internet).

Based upon principles of decentralization, open protocols, greater user interaction and enhanced levels of certified digital ownership, Web 3.0 leans heavily into technologies such as Blockchain (digitally distributed, decentralized data ledgers), smart contracts and digital financial instruments (such as crypto-currencies and NFTs).

These foundational technologies offer end-users greater rights and participation in financial transactions, more interactive retail, gaming and entertainment experiences, and social media platforms that blend virtual and physical environments in a more intuitive and seamless way. The ecosystem that is the nexus of these experiences is increasingly referred to as “The Metaverse”.

Though still nascent, far from cohesive and with some of its impacts possibly over-stated, The Metaverse and Web 3.0 could still be a significant inflection point in internet utility, enabling disruptive new online business models.

Inflection point in internet utility or “just” a massive M&A market?

The question of whether The Metaverse will represent an inflection point in internet utility is up for debate. Many major retailers and brands are trying to size up the opportunities Web 3.0 affords and how to respond to them strategically; creating new modes of customer engagement, partnering with gaming and entertainment companies to create offerings in potential new virtual market-places, which require new marketing and advertising tech capabilities.

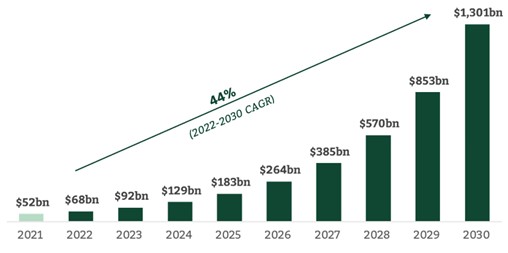

Inflection point or not, the market is already material and attracting significant investment. According to a recent study by Precedence Research, the size of this market could be in the region of $1.3tn by 2030.¹

¹Source: Precedence Research, September 2022

If the prospect of The Metaverse is bringing the worlds of entertainment, gaming and retail into a new paradigm, then 3D/CGI content creation will be a serious enabler. Companies whose tech platforms and pipelines incorporate these capabilities will increasingly be of interest to brands, entertainment and games companies while also rapidly becoming a significant driver of competition and differentiation amongst agencies, VFX and CGI studios.

Although the necessary standardization required to make 3D interoperable across the web isn’t available yet, providers of game engine software, real-time rendering, IT hardware and cloud computing are all vying to establish a plan for Metaverse 3D graphics ubiquity. One example of this is the Khronos Group (a consortium of leading companies in the world of 3D graphics) with members such as AMD, Epic Games, Autodesk, Meta and Microsoft among many others and who’s motto is “Render Everything Everywhere”.

Significant investment followed by a prolonged period of M&A

Assuming that Metaverse adoption continues apace, there will be an unprecedented wall of expertise required to service demand. Brands, entertainment companies as well as advertisers all need to have the ability to create and deploy content in Web 3.0.

Skills in virtual world creation will have increasing value in the supply chain, making tech-focused creative companies a prime target for acquisition and portfolio growth. To that end, services companies such as Accenture, WPP and DEPT are all placing significant bets on its success.

Accenture has already launched Metaverse Continuum Group, an 800 person (and growing) strong division helping clients in areas such as extended reality, blockchain, digital twins and edge computing.

The next generation of the internet is unfolding and will drive a new wave of digital transformation far greater than what we’ve seen to date, transforming the way we all live and work.

Paul Daughtery, Group CEO of Technology and CTO of Accenture

WPP’s specialist creative content production company, The Metaverse Foundry, through Hogarth, develops brand experiences in The Metaverse delivered by a global team of over 700. In parallel they announced a technology partnership with Epic Games, training employees in technologies such as Unreal Engine for 3D creation and virtual production.

Our clients are already seizing the opportunities to connect with their customers presented by The Metaverse, and seeking partners who can bring experiences to life in the most creative and compelling ways.

Mark Read, CEO of WPP

Global Digital Services group DEPT, who JEGI CLARITY raised capital for from Carlyle Group in 2020, launched their 300-person Web3/DEPT offering dedicated to The Metaverse, blockchain technology and NFT services, with a stated intention to derive 20% of group revenues and growing divisional headcount to 1,200 people by 2025.

With all this investment there is no doubt that acquisitions will follow, and we are already witnessing the start of a wave of M&A, with TechMonitor estimating well over $100bn of related M&A in the last two years alone:

Match Group paid $1.7bn for Hyperconnect, a South Korean social discovery and video tech company with whom it is developing “Single Town” a virtual space where singles can meet.

Unity Technology acquired Weta Digital’s technology division (engineering division, artist pipeline and tools) for $1.6bn, to enable “a new generation of creators to build, transform, and distribute stunning RT3D content.”

Epic Games raised $2 billion for Metaverse Endeavor from Sony Group Corporation and Kirkbi (family behind LEGO) in a deal that values the Fortnite creator at $31.5bn,to help fund the kid-focused metaverse content in partnership with LEGO.

Tencent raised its stake in games developer Ubisoft, valuing the business at $10bn, with funds used to leverage existing IP in the metaverse; and probably the largest metaverse-related investment to date.

Microsoft’s government contested acquisition of Activision Blizzard for $69bn as their own “building block for The Metaverse.”

Growth Catalyst Partners is building out a design agency focused on the Metaverse through bolt-on acquisitions for their platform Journey. In 2022, they acquired leading agencies in digital and physical experiences (Squint/Opera and ICRAVE), voice (Skilled Creative) and metaverse/gaming/Web3 (Future Intelligence Group and TheDevHouse Agency).

Gaming is the most dynamic and exciting category in entertainment across all platforms today and will play a key role in the development of metaverse platforms.

Satya Nadella, Chairman and CEO of Microsoft

Ones to watch

Conclusion

Although no unifying definition of The Metaverse yet exists, signals clearly show that building or acquiring capabilities in this space is of increasing strategic importance as market opportunities evolve. As a result, we expect to see a material increase of investment from both industry participants e.g. marketing groups, content producers and consultancies, as well as from financial investors looking to ride positive sector tailwinds and build the next generation of Web 3.0 related products and services.

Equally, there will be increasing demand and expectations made of the technology platforms that this content will sit on. Current early movers such as Decentraland, The Sandbox, Epic and Meta are likely to be challenged as demands for real time rendering across devices become the expected standard.

Once again, expect more investment and M&A as the larger players try to keep up with technological advances.

If you would like to receive copies of our Insights and Reports please click here

JEGI CLARITY Kicks off 2023 with Multiple Promotions

New York, NY, February 9, 2023 – JEGI CLARITY, a pre-eminent M&A advisory firm for the global media, marketing, information and technology industries, headquartered in New York, NY and London, UK, is pleased to announce that the firm has promoted several of their outstanding employees.

Doug Stowe has been promoted to President and COO, managing the firm’s teams and resources, overseeing the firm’s 25+ annual transaction processes, leading talent recruiting efforts and driving short- and long-term strategy.

Rich Kanefsky has been promoted to Managing Director, advising clients on mergers, acquisitions, corporate divestitures and capital raises across the media, marketing services, information and technology sectors. Amanda Cunanan and Kevin Finnegan have both joined the Leadership team this year as Directors. JEGI CLARITY is proud to continue developing the next generation of talent within the firm.

Wilma Jordan, Founder & CEO, North America of JEGI CLARITY, noted, “JEGI CLARITY is very pleased to announce these internal promotions to its Leadership team. As a pre-eminent M&A advisory firm, JEGI CLARITY’s success is built around training our employees on best practices and the most effective protocols that consistently deliver outsized results for our clients. Each of these employees represent a commitment to these client-centric practices and to the successful outcomes our clients expect.”

Author: Adam Gross, Managing Director at JEGI CLARITY

Many private equity funds that traditionally lead leveraged buy-out (LBO) transactions for majority control of companies are creating “Special Opportunity” or “Structured Capital” funds to provide middle-market companies with flexible financing solutions, offering founders and CEOs with an opportunity to raise capital quickly to solve financing needs. These investments are typically structured as minority investments, and the capital can be used by founders/CEOs to solve short-term financing needs, invest in growth initiatives, and/or invest in operations.

Many times, these financing solutions can address situational complexity, from companies seeking capital to pay down debt, to businesses experiencing difficulty securing capital from their usual sources. Furthermore, these solutions can aid founders/CEOs who are seeking to opportunistically invest to support growth in their businesses, without having to give up control of their companies.

One interesting solution for middle-market companies is “Structured Preferred Equity”, an innovative way for companies to raise capital without diluting their ownership stake as much as they would with traditional debt or equity financing. This can be especially beneficial for founders/CEOs who want to maintain control of their companies, while raising capital in a relatively short time – typically within four weeks. For investors, this type of equity investment can provide more robust protection than traditional common equity, which enables investors to move faster in providing the financing, given the lower risk profile.

Here are the general terms and types of structured preferred equity a founder/CEO should expect:

Interest – preferred equity offers the investor an interest payment typically paid as Paid-in-Kind (PIK) interest, which accrues over time and is paid at a later date; this enables the company to conserve cash and utilize that cash for operational investments and growth initiatives; current market rate is in the low double-digit percentage range

Liquidation Preference – preferred equity may provide downside protection to the investor by guaranteeing a certain level of return, before the common equity is paid; for example, a 1.25x liquidation preference guarantees the investor a 1.25x return on their investment before the common shareholders receive any payment

Participating Preferred – typically, this type of preferred equity provides downside protection via a liquidation preference, while also offering the investor the opportunity to participate in the common equity value of the company; as such, once the preferred equity investor receives its interest payments and guaranteed return, it then participates in the common equity waterfall, enabling it to partake in the company’s upside

Convertible Preferred – in this type of preferred equity, the investor chooses either the preferred value of the security or the converted value of the common shares; basically, the investor chooses between the greater of the two calculated values, providing the investor with downside protection, as the minimum value is the preferred value, while offering the investor the option to participate in the company’s upside via the common equity

A few things to consider, structured preferred equity can be more expensive than traditional debt or equity financing, as investors typically demand a higher rate of return for this type of investment. Structured preferred equity can also limit the flexibility of the company, as the terms of the preferred stock may include certain restrictions on the company’s operations or decision-making.

Another important aspect to consider is that structured preferred equity is typically not for companies that are in very early stages of development. It’s more suitable for companies that have a track record of generating revenue and profitability and are looking to expand/invest in growth.

In Conclusion

Structured preferred equity can be a highly flexible, fast and effective way for companies to raise capital. It’s important to understand the pros and cons before deciding, and experienced investment banking professionals will help you understand this financing option and opportunity better, can introduce an array of firms that offer this type of financing solution and will help companies and founders align with the best partner at the best terms.

If you would like to discuss further please click here