PE-backed Dennis Publishing buys car throttle

Dennis Publishing, backed by Exponent Private Equity, has acquired Car Throttle, a digital content brand for car enthusiasts. JEGI CLARITY advised Car Throttle on the transaction.

Dennis Publishing, backed by Exponent Private Equity, has acquired Car Throttle, a digital content brand for car enthusiasts. JEGI CLARITY advised Car Throttle on the transaction.

Future plc, the global platform for specialist media, confirms the completion of the acquisition of SmartBrief, Inc. SmartBrief was advised by JEGI CLARITY, an independent investment bank focused on media, marketing, information and technology, on this transaction.

We examine H1 2019 M&A activity in the Marketing Services sector, a recap of recent JEGI CLARITY transaction activity in the Marketing Services sector as well as recent news and events form across the firm.

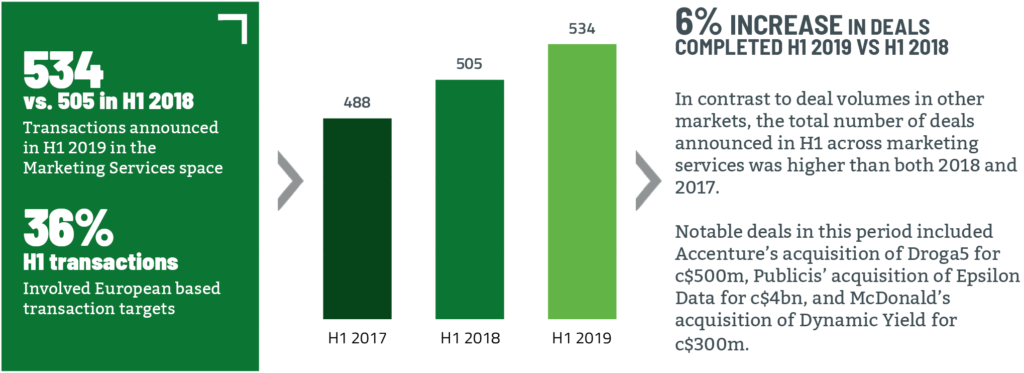

Accenture were the most active acquirer in H1, announcing 7 transactions in H1 2019 compared to 4 in H1 2018, which included the acquisition of Hjaltelin Stahl, Denmark’s leading independent agency, a deal on which JEGI | CLARITY advised.

Of the Global Networks, Dentsu was the most active in H1 with 5 transactions announced.

These included the acquisition of Filter, a US based ‘in-housing’ user experience agency. Financial buyers were more active in H1 2019 compared to H1 2018, as they continue to see the opportunity to build and scale platforms.

The marketing services sector to remain resilient in the face of a broader M&A market slowdown, pointing to the ongoing strategic need for international buyers to build capability sets in digital, data and content. Likewise we’d expect PE activity to continue in this sector as they ride the wave of digital transformation and look to build acquisition platforms.

Design Shanghai and Design China Beijing were acquired by Clarion from Media 10, which was represented by JEGI CLARITY in the negotiations.

We examine the drivers behind the Events Services market and M&A in the space; an interview with Kathleen Thomas on the Events Services sector; our experiences across Events and related services as well as other news and events.

The Events Services sector spans event design/creative, content development, design and fabrication, installation, digital activation as well as event logistics.

Event organisers are increasingly looking to be creative and deliver better experiences and ROI for all participants. In response we have seen events service providers look to consolidate what has been historically a fragmented market. Some of the key strategics such as Freeman and VIAD Corp have been highly active in recent years.

Given the size of the market, the abundance of relatively cheap capital and the opportunity for ‘Buy and Build’ strategies, private equity remains active within the category. Examples of private equity backed platforms include Blackstone’s PSAV, EMZ and Indigo backed MCI Group, and Carlyle backed NEP.

Founded in 2000, MeritDirect of Rye Brook, N.Y., provides marketing services and products that aim to help customers monetize data better. JEGI CLARITY represented MeritDirect in this transaction.

We examine Private Equity activity in Europe, including interviews with leading Private Equity funds Accel-KKR, Exponent, Livingbridge and Waterland.

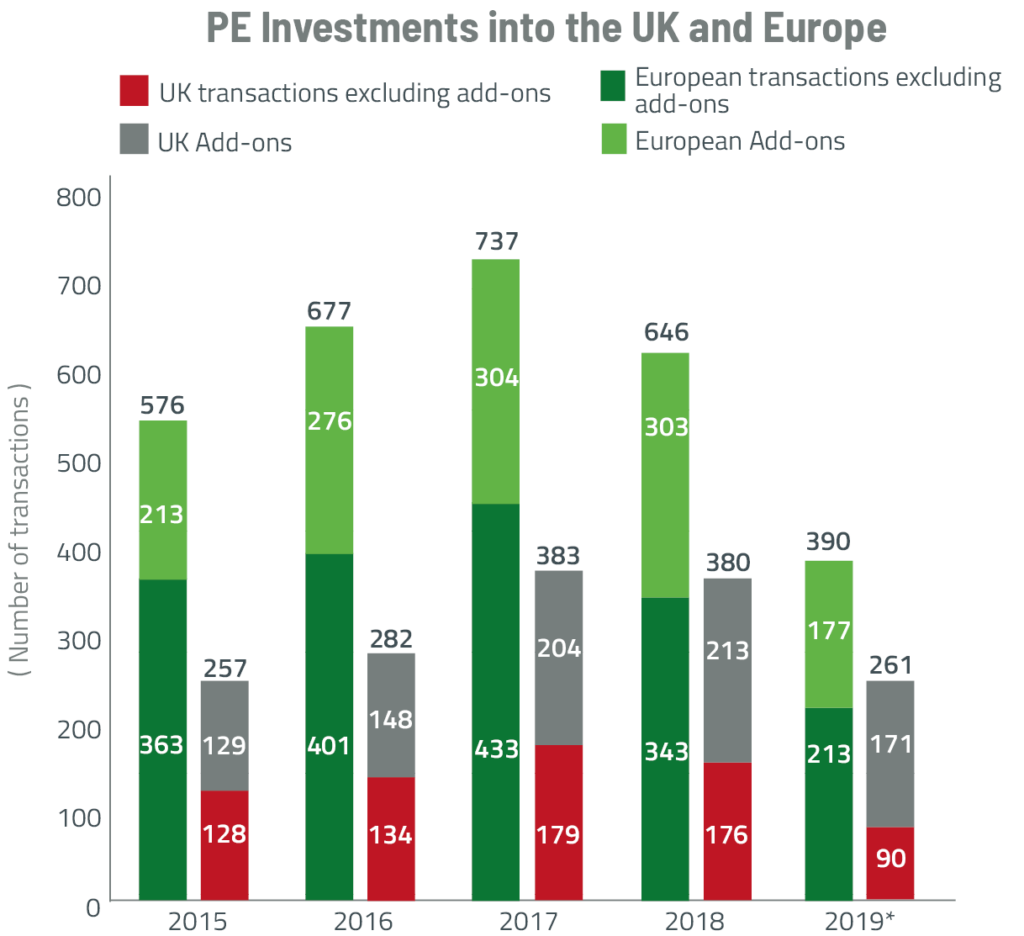

Cumulative dry powder in Europe

Dry powder remains strong but with increasing capital chasing fewer transaction opportunities.

Decrease in transaction volume Q1 2018 to Q1 2019

Macro headwinds, in particular Brexit volatility and risk are slowing transaction volumes across Europe.

Proportion of total private equity investments that are add-ons in 2019

Increasingly Private Equity funds are focussed on building value in existing portfolio companies.

“Overall, we are long the UK. Brexit has given us a more aggressive stance to deploying capital in the market.”

“At the moment we are decidedly more predisposed to business with an international footprint rather than businesses solely dependent on the UK economy and so less exposed to cyclical downturn.”

“Brexit hasn’t impacted our appetite for investing. We invest in high growth businesses in the mid-market which are often disruptive in niches and as such we are comfortable that they can grow irrespective of the political and economic situation.”

“From an investment perspective, as we do invest in the UK, Brexit has not affected our overall appetite to invest in the UK or elsewhere.”

New investment in Q1 2019 was 37% down on Q1 2018.

Uncertainty around Brexit and further macroeconomic factors across Europe have contributed to slowing transaction volumes as sellers wait to see a more stable market to transact and buyers have to work harder to navigate the investment landscape.

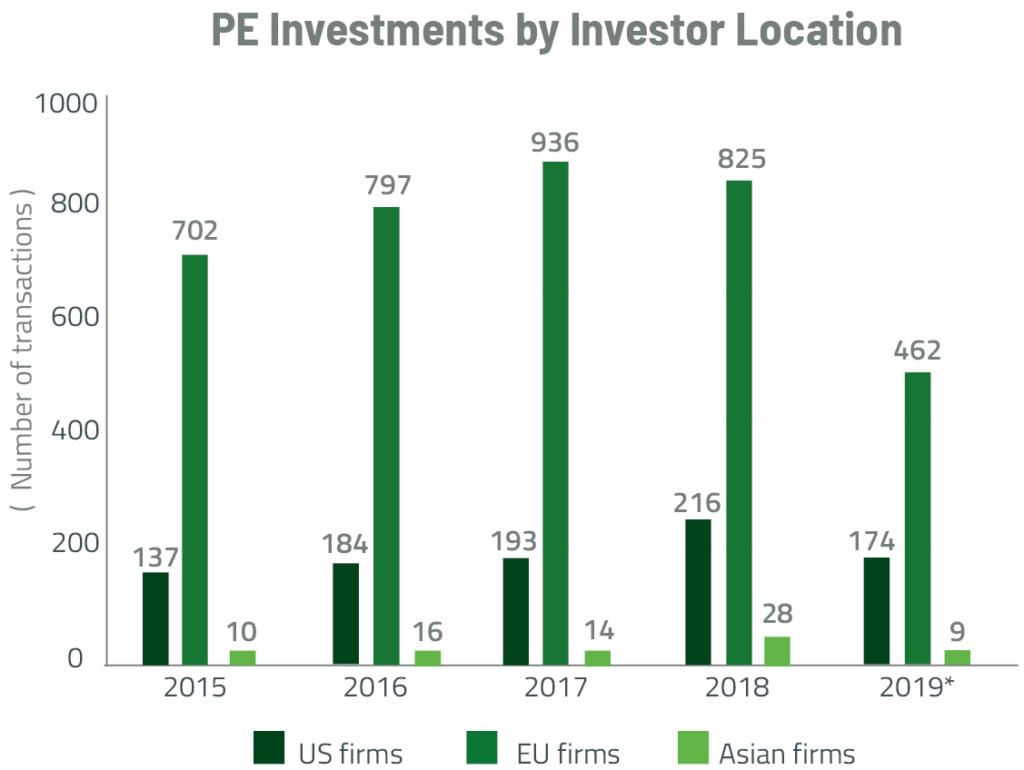

With the US markets growing ever more competitive US firms are increasingly deploying capital in European companies.

• The proportion of total investments in European firms by US investors has increased from 16% in 2015 to 27% in 2019

• Decrease in the proportion of investments made by European firms from 83% in 2015 to 71% in 2019

This month we examine Q1 2019 European media and technology M&A activity; current perspectives on Europe from US buyers and investors; key takeaways from Q1 activity across our sectors and other news.

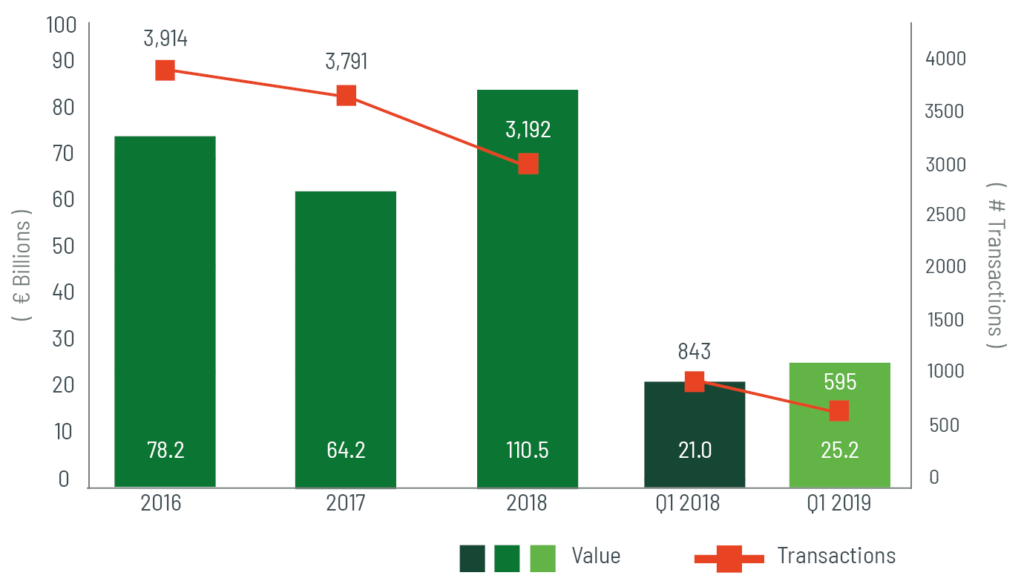

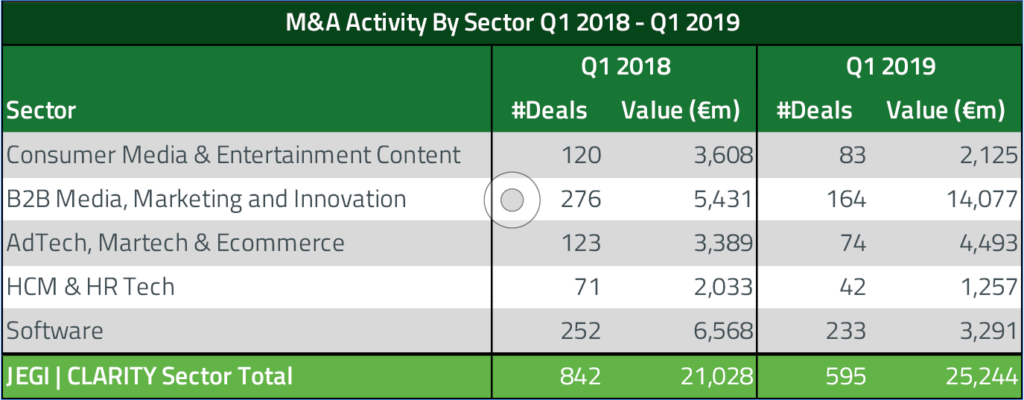

2019 recorded a strong start for M&A deal activity in our sectors with 595 transactions announced in Q1. Whilst we saw a 20% drop on the previous year’s Q1 deal volume, deal value was up 20% with a total of €25.2 billion in the quarter, fuelled in part by ‘mega-deals’ including NEC’s €1.4bn purchase of Danish IT services provider KMD.

The B2B, Media, Marketing and Information sector saw the largest deal of the quarter, a €5.7bn acquisition of Scout24, a public German-based Internet Software company, by Hellman & Friedman and The Blackstone Group.

Consumer media and entertainment content continues to see high levels of M&A activity and peaking valuations, reflecting the shifts in media consumption as demand for content shows no signs of slowing. Roper Technologies’ €475m acquisition of Foundry.

Globally we continue to see high levels of M&A activity in consumer media and entertainment content, reflecting shifts in media consumption, and in turn, strategies for audience monetisation. Entertainment content remains an area where demand for video production technology and services continues to grow.

Software is still dominating transaction activity within JEGI CLARITY sectors. Notably in the US in Q1 was SAP’s acquisition of CX analytics software company Qualtrics for c$8bn for a business which generated c $400m in revenues in 2018. In Europe activity echoed this, with one example being Nordic Capital’s acquisition of business intelligence and analytics software provider BOARD International in an estimated $500m transaction.

In-housing of adtech/martech and direct-to-consumer digital marketing capabilities continues to drive transactions in Q1 2019. McDonalds Corporation’s c$300m acquisition of Dynamic Yield, an AI-powered personalisation and data management platform is evidence of this.

In-housing of adtech/martech and direct-to-consumer digital marketing capabilities continues to drive transactions in Q1 2019. McDonalds Corporation’s c$300m acquisition of Dynamic Yield, an AI-powered personalisation and data management platform is evidence of this.

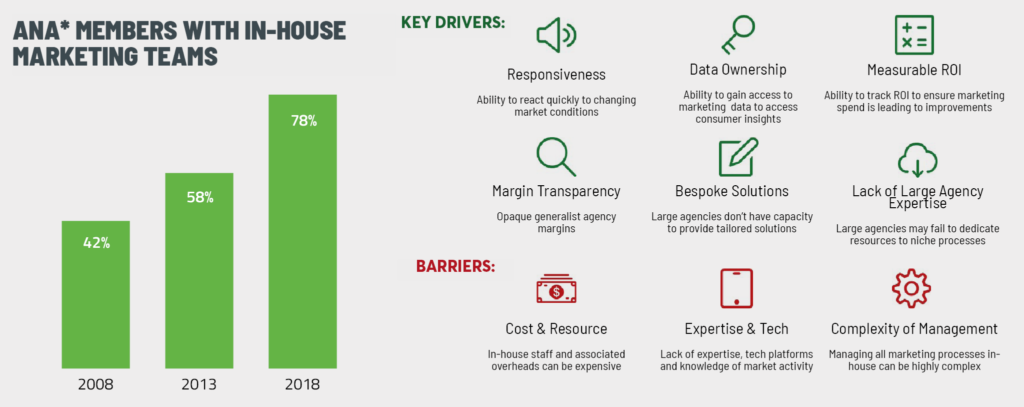

This month we examine the digital marketing industry including the key current drivers of growth, why brands are increasingly ‘In-Housing’ and global M&A activity in the sector.

Brands are seeking greater control of digital marketing as this is increasingly viewed as a sales channel as much as a marketing channel.

Global M&A activity in performance marketing services has increased in recent years. The growing digitalisation of media and rising digital ad costs are driving consolidation in the sector.

• Whilst the Global Networks continue to be most acquisitive in this space, consultancies (such as Accenture) and PE-backed platforms (such as Elite SEM and Wpromote) were also prominent.

• We expect M&A to remain active in 2019 with several acquisitions already announced including the investment in leading technologyled marketing agency, Brainlabs, by private equity fund Livingbridge (JEGI | CLARITY advised Brainlabs on this transaction).

Livingbridge has made an investment in London-based Brainlabs, a marketing agency. JEGI CLARITY represented and advised the shareholders of Brainlabs on the transaction.